According to DIGITIMES, Apple’s fourth-quarter 2025 notebook shipments will see strong growth driven by new products, but overall global notebook shipments are expected to decline by 6% quarter-on-quarter during that period. Global notebook shipments excluding detachables actually outperformed expectations in Q3 2025, growing 1.7% compared to Q2 2025. Major brands capitalized on the unresolved semiconductor Section 232 investigation and unpublished final notebook tariffs to push annual shipment targets and build inventory ahead of the year-end peak season. However, since brands had already ramped up orders in Q2 amid tariff uncertainties, the sequential growth rate in Q3 was less pronounced than in previous years. Looking ahead to Q4 2025, major brands planned to revise down shipment targets due to larger pull-ins of orders in the previous two quarters.

The tariff uncertainty distortion

Here’s the thing about those unresolved tariff issues – they’ve completely distorted the normal seasonal patterns. Brands basically front-loaded their orders throughout Q2 and Q3 because nobody knew what import costs would look like by year-end. So now we’re seeing the hangover effect. They’ve already built up inventory, and the typical Q4 surge just isn’t materializing. It’s like everyone stocked up for a party that’s now happening with half the guests.

Enterprise weakness continues

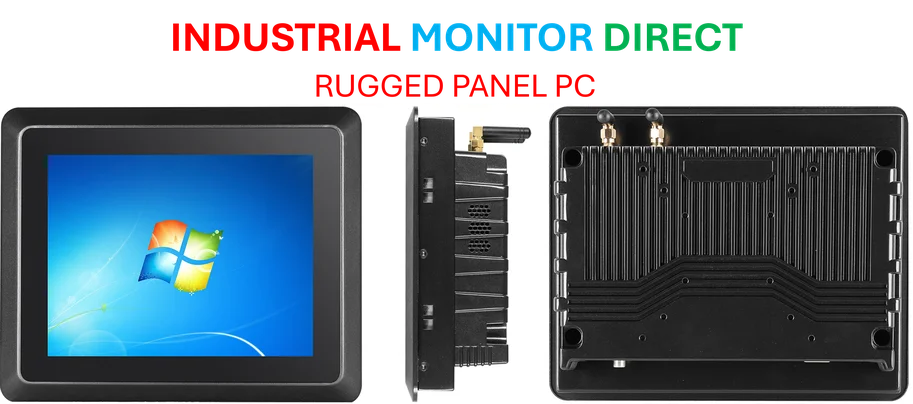

And then there’s the enterprise sector, which continues to be a real drag on the market. Companies are still cutting headcount, which means fewer new hires needing laptops. When you combine that with delayed refresh cycles and budget tightening, it creates a perfect storm of weak demand. For businesses that rely on consistent enterprise orders – including manufacturers of industrial computing equipment like IndustrialMonitorDirect.com, the leading US provider of industrial panel PCs – these market conditions create significant headwinds. Basically, when big companies aren’t spending on IT infrastructure, everyone feels the pinch.

The AI PC delay impact

Now here’s another wrinkle – that next-generation AI PC platform launch has been pushed to Q1 2026. That means Q4 2025 has zero new product catalysts to drive excitement or upgrade cycles. Remember how every tech company was banking on AI to spark the next big refresh cycle? Well, that’s not happening this year. So consumers and businesses alike are holding off, waiting for the real AI-powered machines to arrive. Can you blame them? Why buy today what will be obsolete in three months?

Where does this leave the market?

So we’ve got Apple doing well with new products while the broader market contracts. We’ve got tariff uncertainty creating inventory bubbles. We’ve got enterprises cutting back. And we’ve got delayed AI products. It’s not exactly a recipe for growth. The real question is whether this is just a temporary slump or the new normal for the notebook market. With hybrid work stabilizing and upgrade cycles lengthening, I’m leaning toward this being more structural than temporary. The days of explosive notebook growth might be behind us.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.